Quarterly Commentary - Q3 2022

|

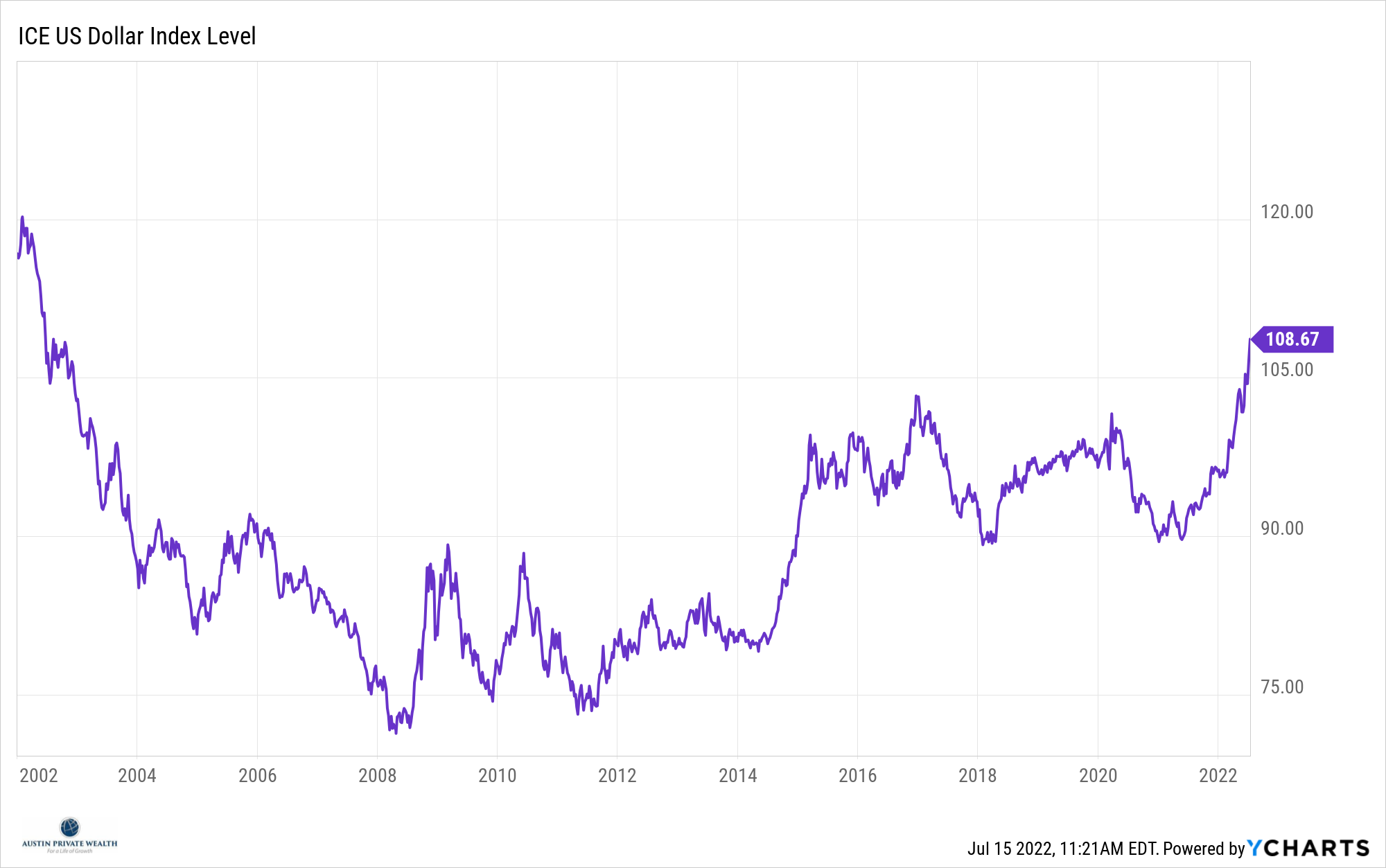

Q2 2022 Review (For Text, please continue to scroll through this page)

Source: Ycharts

The first half of 2022 was one of the worst January to June periods for both stocks and bonds ever, as declines continued unabated from an already poor first quarter. Inflation continues to soar, with a year over year growth rate of 9.1% as of this writing. The Federal Reserve in response has started to accelerate rate hikes with a large 0.75% increase to the Federal Funds rate at the last meeting. The old adage “Don’t fight the Fed,” seems as apropos as ever. Virtually all assets globally, with the obvious exception of commodities, have plummeted in response. Another major development this year is the rise of the U.S. dollar against a basket of major global currencies. It is now at levels last seen 20 years ago.

Austin Private Wealth Model Changes

Outlook It is impossible to discuss the market outlook without first addressing the elephant in the room – inflation. There are 3 primary inputs that can contribute to inflation:

One point that is often overlooked in our partisan political environment is that the current inflation is a global phenomenon. Much of that is driven by the supply chain issues caused by COVID lockdowns in China and the Russia/Ukraine War. Had these things not happened, while inflation would still be trending upward, it is unlikely that the US or any country would be reaching 40-year inflation highs. Nonetheless, the final Biden Administration stimulus package (which was $1.9 trillion in 2021) along with the Federal Reserve’s incredibly slow policy change, left United States with massive, excess liquidity. In retrospect it seems obvious that the convergence of NFTs selling for tens of millions of dollars, meme stocks trading at stratospheric prices, and incredibly sketchy SPAC deals getting oversubscribed on Wall Street, was the blinking neon sign of a market top. Finally, demand has only just started to abate. Take a look at this chart that shows the massive increase… roughly 40% in two years in US imports. Many believe that inflation is near a top and that already the Federal Reserve’s actions are pulling so much liquidity out of the system that demand is being crushed and a recession looms. Some commodity prices such as lumber are down substantially from their recent highs. Other important inputs like semiconductor prices have started to come down. Even the powerful US residential real estate market appears to have cooled in the past 60 days. And for US consumers, the strength in the dollar also appears to be helping a lot. We believe that the cooling of inflation is not a switch that turns on and off and will likely stay high through the 3rd quarter as lower readings in Q3 2021 fall off the calculation. It takes time for the economy to shift gears and the labor market is still very strong. This makes us maintain our cautious view on bonds. While rates have gone up and value has improved, the risk/reward still does not appear very attractive in most categories. Equity markets on the other hand have significantly repriced, and now appear closer to a bottom. The exact timing is impossible to forecast. Q2 earnings have just started and will likely take down 2022 earnings estimates and beyond. That will put near-term downward pressure on stocks. Given the historic economic forces at play it would not be surprising to see a decline of another 10% from here. Further, if you believe as we do, the mantra we mentioned at the beginning of this commentary, “Don’t fight the Fed” then we also need to see the Fed stop tightening financial conditions (or the market to believe that they will soon) before an equity market recovery can start in earnest. For those with a long-term outlook, prices are starting to look much more attractive. We expect to look for opportunities for our investors to increase equity exposure as prices fall from here. It is essential to remember at times like these, that prices only fall because of all the gloom and doom, but ultimately companies make changes, government policies adjust, confidence improves… and stocks recover and grow. One final thought, a collapse in consumer sentiment is one historically good indicator of a market bottom. As sentiment is at its worst, the seeds of a stock market recovery are usually just beginning. It’s not a perfect indicator, but pretty good. Below is a snapshot of the last 50 years. In fact, the recent readings are the lowest in the history of the survey going back even further! That bodes well for future stock prices.

Austin Private Wealth, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Austin Private Wealth, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Austin Private Wealth, LLC unless a client service agreement is in place. | |||||||||||||||||||||

|

|